Image by Worldclassphoto on Shutterstock

As demands for credible climate action rise, so do expectations for companies to inventory and address their Scope 3 greenhouse gas emissions – those that are outside of their direct control that occur upstream and downstream in their value chains.

In this blog, we explain how to get started on taking credible action on Scope 3 emissions.

Rising expectations

Scope 3 has been pushed into the spotlight. Businesses are under increasing pressure from customers, investors, lenders, insurers, and regulators to measure scope 3, set targets, take credible action to decarbonise their value chain, and disclose their progress.

With corporate net-zero target setting fast gaining momentum, an increasing number of organisations are either setting or committing to set Scope 3 emissions reduction targets and engage value chain partners to do the same. Customers are seeking out suppliers that can help them to reduce their supply chain emissions. Financial institutions and insurers are considering their own financed emissions using the Global GHG Accounting and Reporting Standard for the Financial Industry. Companies that make progress in reducing their value chain emissions may benefit from better financing and insurance rates (or avoid higher ones).

In 2023, the International Financial Reporting Standards (IFRS) issued IFRS S2 Climate-related Disclosures, which requires companies to disclose absolute gross GHG emissions generated during the reporting period, measured in accordance with the GHG Protocol, including scope 1, 2 and 3 GHG emissions. It is up to individual jurisdictions worldwide to adopt and/or adapt the standards issued by the ISSB, however, G20 countries have signaled their support for the new IFRS standards. The EU’s Corporate Sustainability Reporting Directive also requires companies in scope to disclose their absolute gross scope 3, subject to materiality and other reliefs/ exemptions.

That means that all companies, no matter the size, need to:

build their understanding of scope 3;

understand rapidly rising expectations around measuring, disclosing, and addressing scope 3; and

understand what it looks like to take credible action

What are Scope 3 emissions?

Your scope 3 emissions derive from activities outside of your company’s direct control, upstream or downstream in your value chain. While these emissions are a consequence of your activities and decisions, they occur in sources that are owned or controlled by other entities. In most sectors, scope 3 makes up the vast majority of a company’s overall carbon emissions inventory and is significantly larger than its scope 1 and 2 emissions combined.[1]

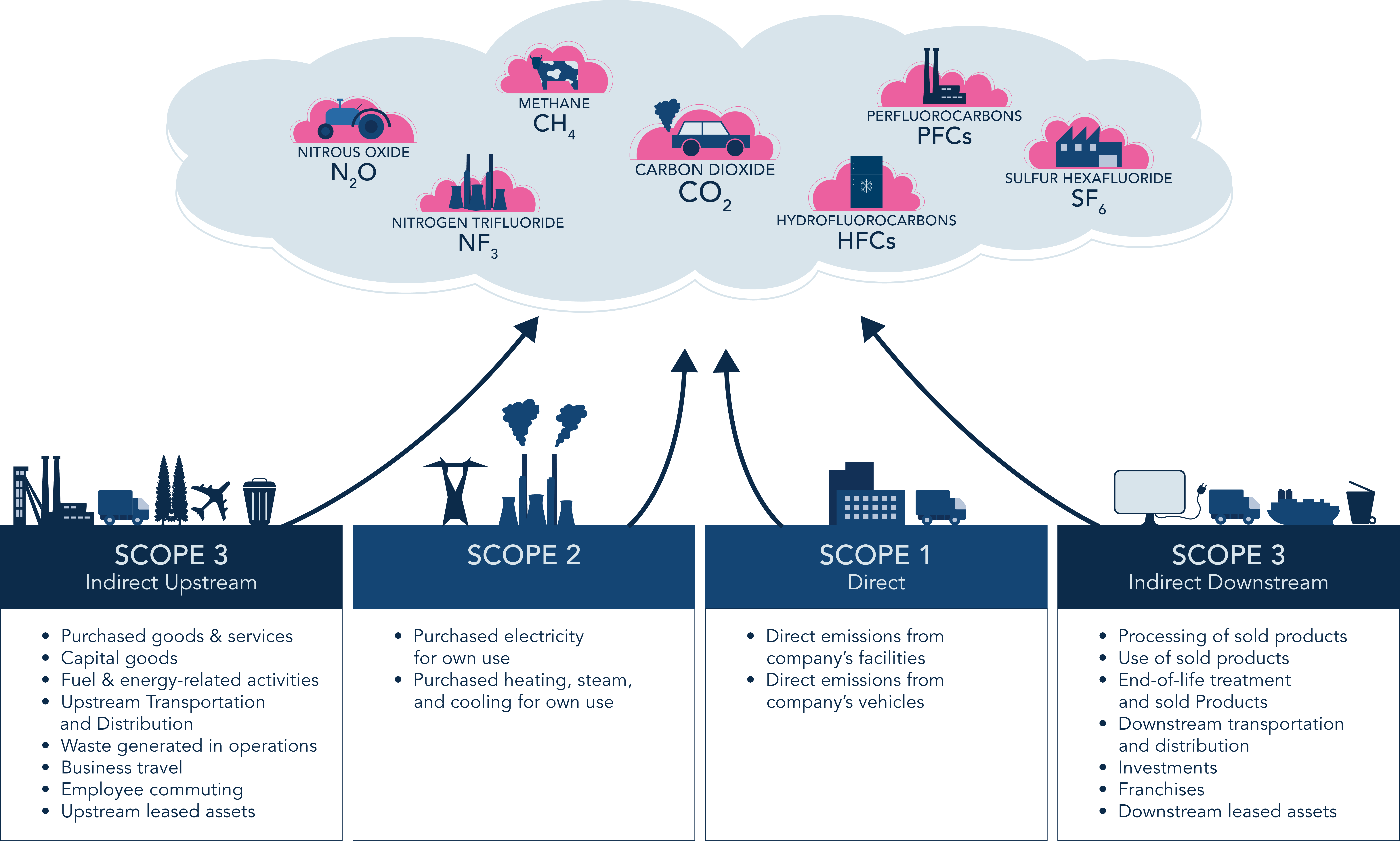

The world's most widely used set of greenhouse gas (GHG) accounting and reporting standards, the Greenhouse Gas Protocol, groups emissions into three scopes:

Image: Scope 1, 2, and 3 Greenhouse Gas Emissions (adapted by Embedding Project from GHG Protocol)

Scope 1: Direct emissions from sources that are owned or controlled by a company (includes emissions from production and industrial processes, refrigerants, combustion in boilers or furnaces, and emissions from company owned vehicles.

Scope 2: Indirect emissions from a company’s purchased or acquired electricity, steam, heat, and cooling.

Scope 3: Indirect emissions resulting from a company’s activities, occurring upstream or downstream in a company’s value chain.

Taking credible action on Scope 3 emissions

Businesses are under increasing pressure from governments, investors, lenders, and insurers to measure their Scope 3 emissions, set targets, take credible action to decarbonise their value chain, and disclose their progress.

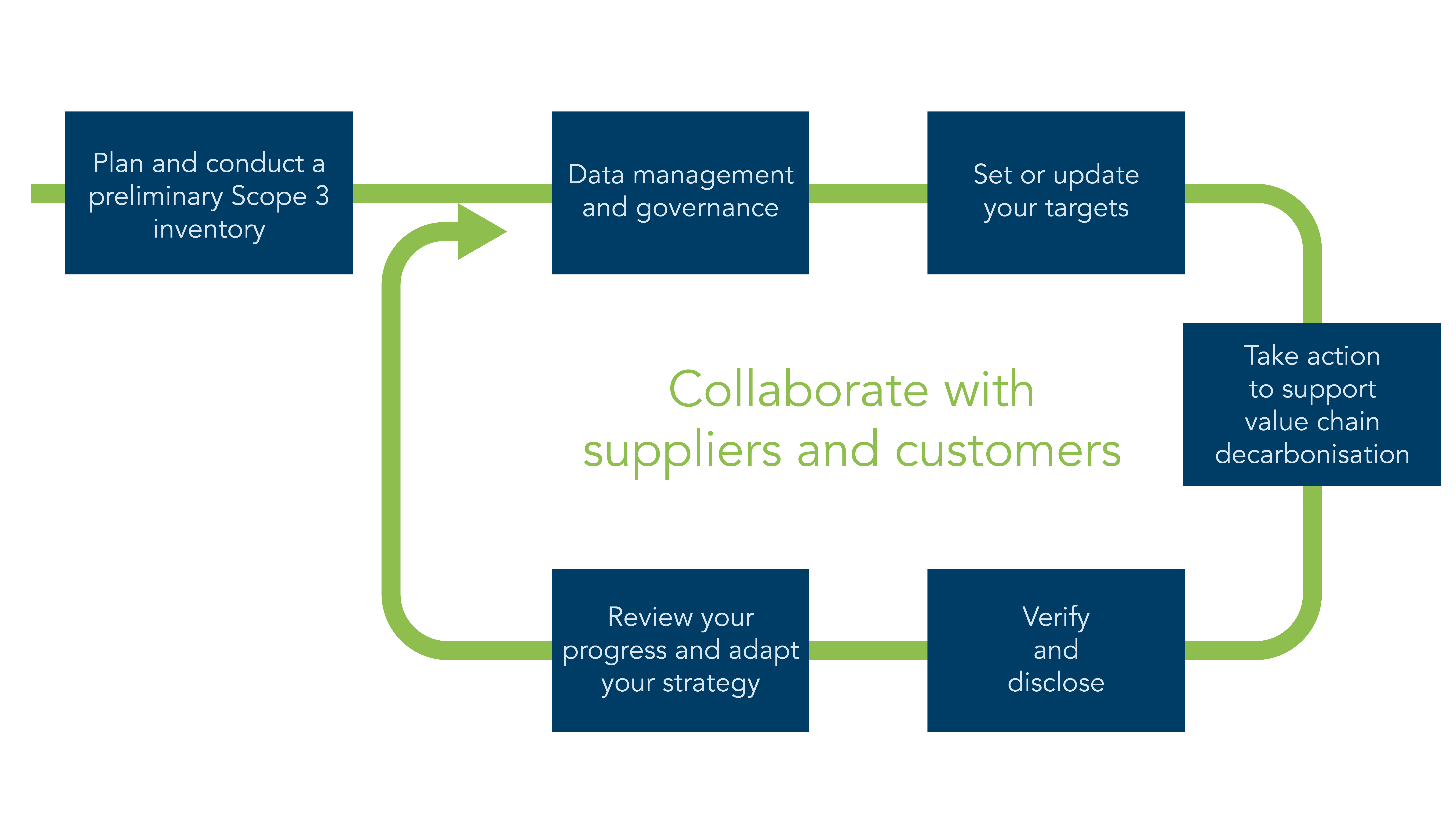

Image developed by Embedding Project

To understand and address your Scope 3 emissions you will need to:

Conduct a preliminary Scope 3 inventory to identify emission hotspots to know where to focus (you will need to define the boundaries of your operations, map out your value chain and undertake a scope 3 inventory, likely starting out by using estimation until you can gather more robust data);

Work to understand supplier and customer maturity and develop a robust data management system;

Set scope 3 targets (and optionally, seek validation of those targets);

Develop a strategy to support your value chain partners’ efforts to decarbonise;

Verify your data and data processes and disclose your progress; and

Adapt your strategy to keep driving down value chain emissions.

All of these actions will require that you collaborate with suppliers, customers, and other value chain partners.

In subsequent years, there will be additional work to be done. You will need to improve your data collection and your understanding of your emissions, update your targets, and continue to invest in collaborating with your value chain partners to identify ways to further decarbonise until you reach your goal.

Given the multi-year timeframe for a company to gather credible Scope 3 data, set credible targets, and put in the place reliable processes and systems, companies should be preparing now for an inevitable future of Scope 3 disclosure.

Our latest guide contains much more detailed information on how to navigate each of these steps. We encourage you to read (and share!) it here: Addressing Scope 3: A Start Here Guide

Further resources

For examples of leading Scope 3 goals in a range of industries, consult our free Sustainability Goals Database.

For support articulating a credible public position consult our guides on Developing Position Statements on Sustainability Issues and Emerging Trends and Best Practice in Climate Position Statementsand our free Position Statement Database.

For additional guidance on climate risk and climate risk oversight, consult our guide on Climate Change and Climate Risk Oversight: A Guide for Corporate Leaders and Directors.

Footnotes

Image by Worldclassphoto on Shutterstock.

1 CDP (https://www.cdp.net/en/research/global-reports/engaging-the-chain); (EPA (https://www.epa.gov/climateleadership/Scope-3-inventory-guidance); Carbon Trust (https://www.carbontrust.com/resources/briefing-what-are-Scope-3-emissions).